04.29.26

The 2026 Multifamily Debt Maturity Wave

A Decision Cycle—Not a Distress Cycle

“The owners who are going to come out of this in good shape are the ones who are proactive, realistic, and have a clear plan — whether that’s refinancing, selling, or bringing in a capital partner,” David Kurrle, Director Real Estate Capital Markets at Regions Bank.

Introduction

As the multifamily industry moves deeper into 2026, the debt maturity wave has become one of the most discussed—and often misunderstood—topics across investors, property owners, and lenders. While much of the national narrative has centered on risk and distress, the reality in Midwest markets such as Chicago is more balanced and, in many cases, more constructive. “Maturity is not a trigger for distress; it is a trigger for decision,” according to Kiser Group’s Dan Gonzalez. Owners are not broadly being forced into action—they are being presented with a set of strategic choices that will shape the next phase of their portfolio evolution.

Understanding the Scope of the Maturity Wave

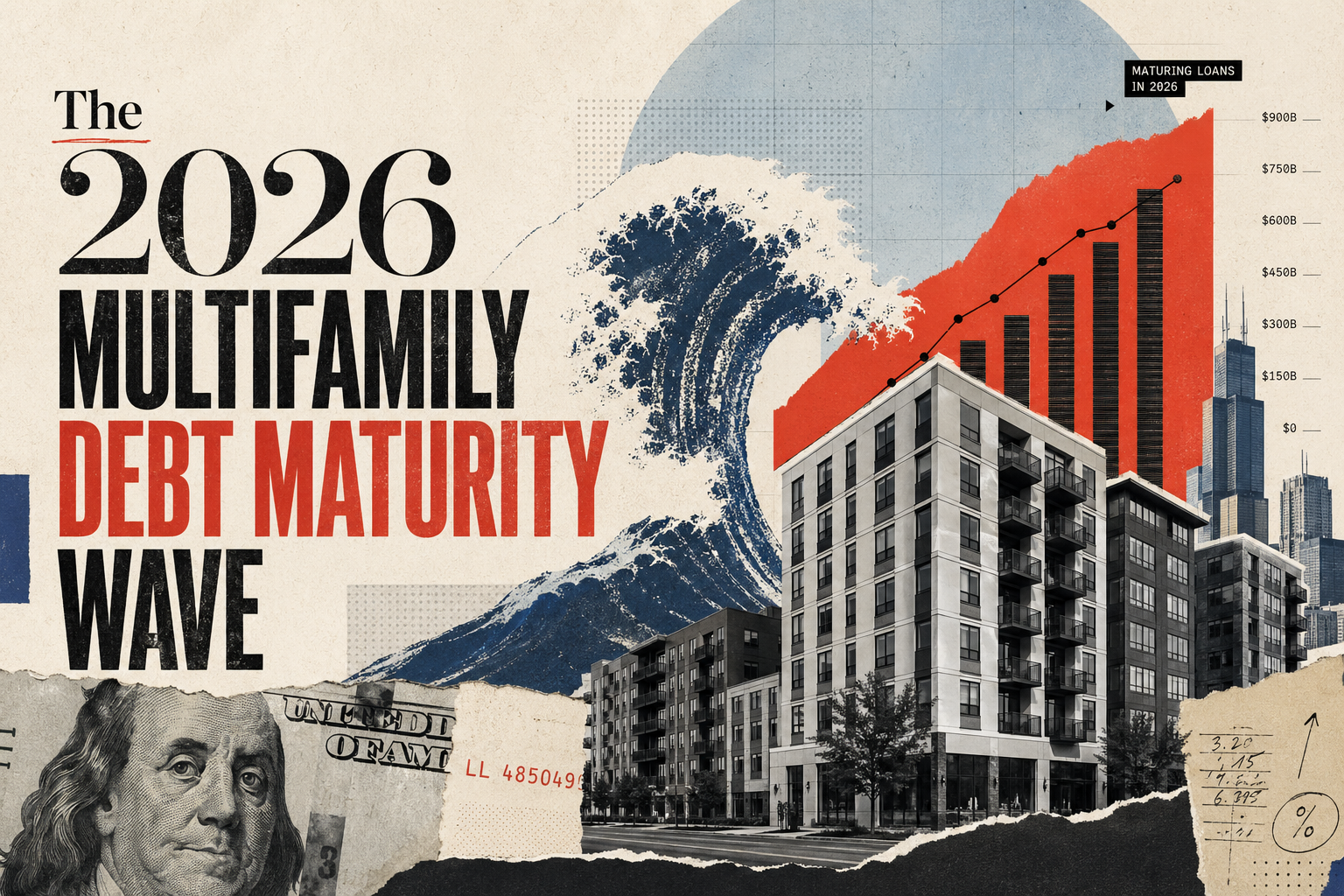

The scale of upcoming loan maturities is significant and should not be ignored. According to Mortgage Bankers Association estimates, more than $875 billion in commercial real estate debt will mature in 2026, following an unprecedented volume in 2025. A large portion of this debt was originated during the 2020–2022 period, when interest rates were historically low and capital was abundant. As these loans reset into a higher-rate environment, owners are facing a meaningful shift in financing dynamics, including higher debt costs, tighter underwriting standards, and in some cases, the need for additional equity due to debt coverage requirements. However, scale alone does not define outcome. The key differentiator in this cycle is that most assets—particularly in the Midwest—remain fundamentally stable. Mike Mosher of Kiser Group notes that “today’s challenge is not broken assets; it is a reset in capital expectations.”

Reframing the Narrative: Why This Is Not 2008

There is a tendency among market participants to compare the current environment to prior downturns, particularly the Global Financial Crisis. However, the underlying conditions today are materially different, and according to Mike Mosher, “the market is not being forced to transact; it is choosing when and how to transact.” Asset-level performance in multifamily remains relatively strong, especially in supply-constrained markets like Chicago. Occupancy levels are stable, rent growth has been resilient, and there is not a systemic collapse in fundamentals. While refinancing may be more difficult, it is not broadly unavailable. Unlike the GFC, capital remains available, albeit more on the sidelines than some owners would prefer. As a result, the expectation of widespread distressed sales and deeply discounted pricing is overstated, specifically in Midwest multifamily markets.

The Core Decision Framework Facing Owners

Owners approaching loan maturities in 2026 are fundamentally evaluating three strategic paths: refinance, recapitalize, or sell. Each path has become more nuanced in the current environment. Refinancing remains viable for well-performing assets but often requires lower leverage and additional capital. The term “cash-in refinance” has become much more common than heard in the last real estate cycle. Recapitalization can provide flexibility where partnership dynamics or capital structures need to evolve. Selling, meanwhile, is increasingly being considered not as a last resort, but as a proactive capital allocation decision—particularly when the cost of refinancing outweighs the benefits of continued ownership. As Mike Mosher notes, “the right answer is not always to hold; it is to optimize capital at the right moment by moving equity to another asset for greater returns.”

A new approach “The Planned Sale”

Approaching this decision cycle through what we call the planned sale is a path to success for many owners. Rather than waiting for maturity deadlines to force action, owners should begin planning disposition strategies well in advance. Dan Gonzalez observes that “the best exits in this cycle will not be forced; they will be planned. We help our clients anticipate, then plan for these transitions.” This approach allows owners to enhance asset performance, evaluate market timing, and create competitive buyer interest—ultimately leading to stronger outcomes. In contrast, reactive sales driven by urgency tend to limit optionality and compress value.

The Real Risk: Loss of Optionality

While the market itself is not broadly distressed, the real risk for owners is delaying action. Waiting too long to evaluate options can significantly reduce flexibility, whether in refinancing negotiations or sale execution. As loan maturity approaches, timelines compress, leverage decreases, and negotiating power shifts away from the owner. The difference between a strong outcome and a compromised one often comes down to how early the planning process begins. “The owners who are going to come out of this in good shape are the ones who are proactive, realistic, and have a clear plan — whether that’s refinancing, selling, or bringing in a capital partner,” according to David Kurrle, Director Real Estate Capital Markets at Regions Bank.

What Owners Should Be Doing Now

In this environment, preparation—not prediction—is the advantage. Based on current market dynamics, there are five immediate actions owners with 2026–2027 maturities should take.

- First, start planning early – 12–18 months ahead of maturity – to create optionality across refinancing, recapitalization, or sale.

- Second, establish a realistic valuation, as understanding true market value is foundational; many owners either overestimate or underestimate their position, leading to suboptimal decisions.

- Third, pressure-test your refinancing scenario by evaluating debt service coverage ratios under current rates, required equity contributions, and lender appetite, and evaluate whether refinancing aligns with long-term strategy.

- Fourth, evaluate asset positioning, as even small improvements in operations, rent strategy, or property condition can materially impact both refinancing outcomes and sale pricing.

- Finally, build a decision framework—not just a transaction plan—by shifting the core question from ‘Should I sell?’ to ‘What is the best capital event for this asset at this point in the cycle?’

Kiser Group’s Approach

At Kiser Group, the role of our brokers has fundamentally evolved in this environment. Our focus is not simply on executing transactions, but on helping clients navigate complex capital decisions with clarity and confidence. This includes providing early-stage valuations, structuring decision frameworks, and advising on the full spectrum of options—from refinancing to recapitalization to sale. By engaging before urgency sets in, we help clients preserve optionality and position themselves for the best possible outcome. As David Kurrle of Regions Bank notes “A broker who can advise with transparency and help borrowers find the best solution to fit their strategic plan is incredibly valuable right now. It’s less about simply ‘running a deal’ and more about being a trusted advisor.”

Conclusion

The 2026 debt maturity wave represents a pivotal moment for multifamily owners, but it should not be viewed through the lens of crisis. Instead, it is an opportunity to reassess, reposition, and execute with intention. Those who approach this cycle proactively—armed with data, strategy, and the right advisory support—will be best positioned to capitalize on it. In today’s market, success will not be defined by who reacts fastest, but by who plans most effectively. Mike Mosher sums it up this way: “in this cycle, preparation is the new alpha.”